Tactically Bullish view on Sea Limited

Sea Limited, the largest internet conglomerate in Southeast Asia, continues to solidify its leadership across key markets. The company maintains a dominant position in e-commerce (60% of enterprise value), gaming (20% of EV), and a rapidly expanding fintech and digital banking segment.

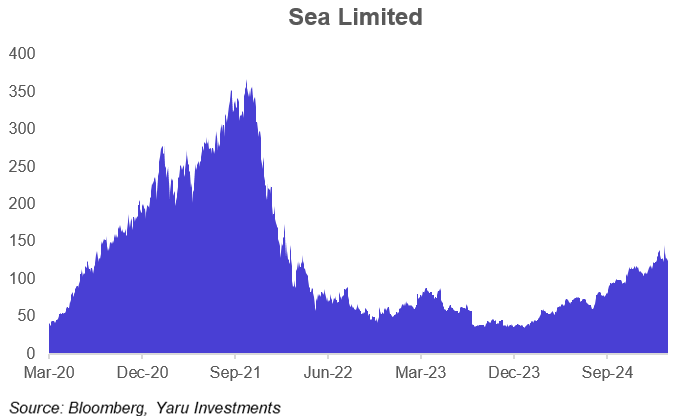

Following a strong Q4 2024, we are increasingly bullish on Sea Limited.

The results highlight stable competition in e-commerce, accelerating growth in fintech, and a resilient gaming business that remains a reliable cash generator.

Despite competition from cross-border platforms, Shopee and Lazada continue to defend their pricing power. TikTok Shop offers lower prices in Indonesia and Malaysia, but Shopee remains more competitive in Singapore.

Meanwhile, the company’s fintech arm is scaling rapidly, with a 60% year-over-year increase in lending users and a loan book expansion of 64% YoY to US$4.6 billion. Notably, credit risk remains well-managed, with non-performing loans steady at 1.2%.

Management remains optimistic about sustained fintech growth, driven by the success of its hyper-localization strategy.

Keep reading with a 7-day free trial

Subscribe to Yaru Investments Substack to keep reading this post and get 7 days of free access to the full post archives.